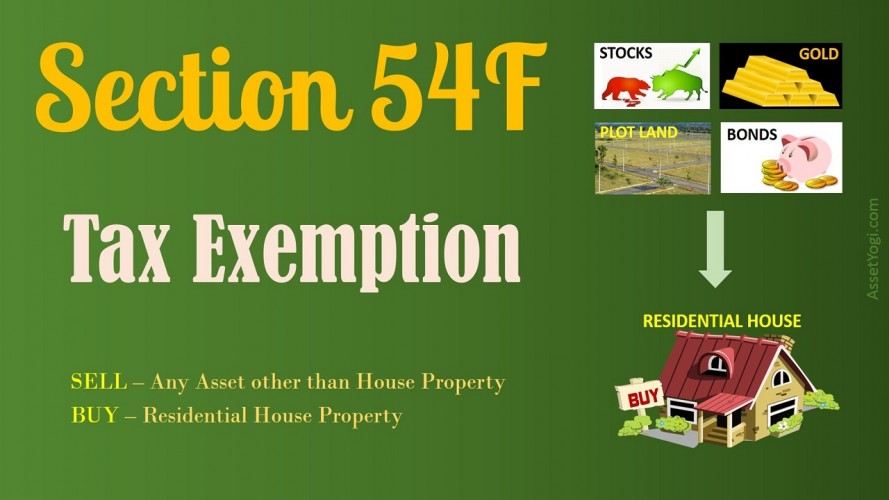

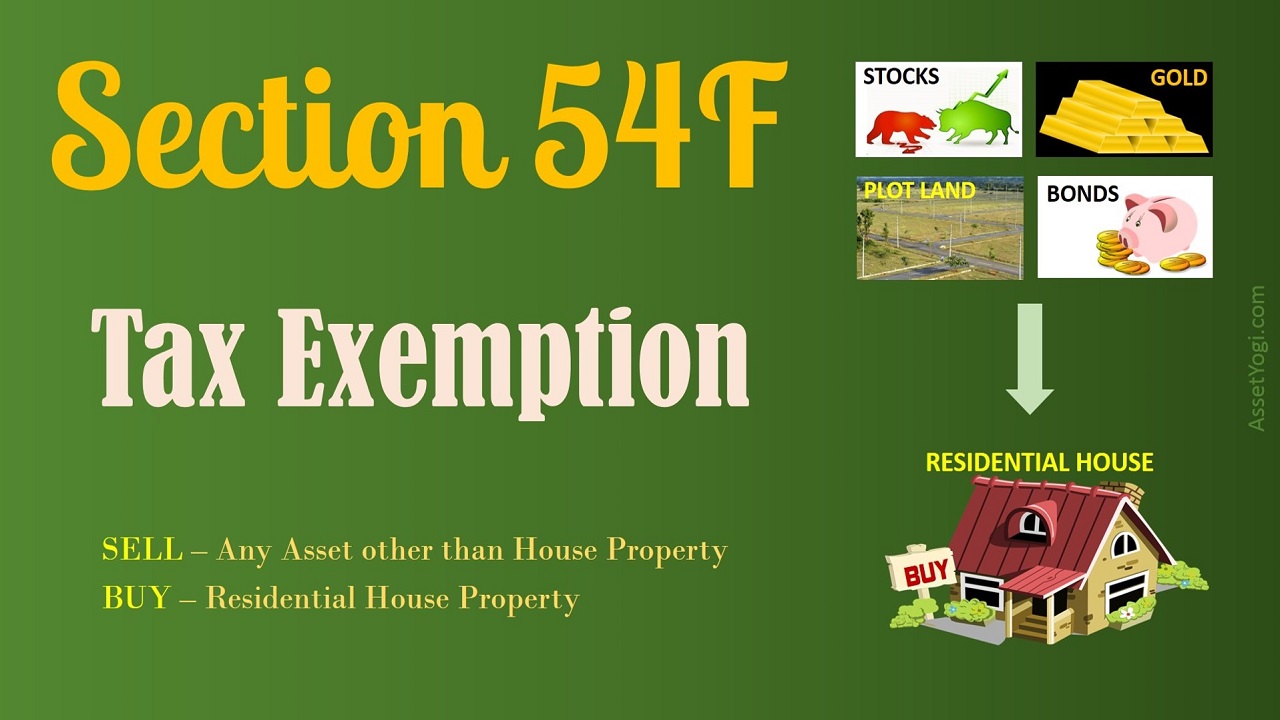

Section 54F of Income Tax Act 1961 provides for tax exemption on capital gains that result from sale of any Long Term Asset (original asset) other than Residential House Property provided that the entire net consideration is invested in

1. Purchase of one residential house property (new asset) within 1 year before or 2 years after the date of transfer of original asset or

2. Construction of one residential house property (new asset) within 3 years after the date of transfer of original asset

For the purpose of Section 54F:

Original Asset – Any long term asset other than house property, such as Stocks, Bonds, Gold, Plot Land etc. that is sold after minimum 3 years from its date of acquisition.

New Asset – Residential House Property bought from sale proceeds of original asset.

Net Consideration – Full value of sale consideration received or accrued as a result of transfer of original asset minus any transfer costs

Exemption Amount under Section 54F of Income Tax Act 1961

- If you invest the entire net consideration of original asset in a residential house, then entire capital gain amount is eligible for tax exemption under section 54F, and

- In case you did not invest the entire sale consideration but only a part in a residential house property, then you can claim exemption only the proportionate amount that is invested in house property. The exemption amount can be calculated by the formula

Exemption Amount = Capital Gain X Amount Invested/ Net Sale Consideration

No Exemption under Section 54F

You will not be able to claim tax exemption under Section 54F of Income Tax Act 1961, if

- You own more than 1 residential house property, exclusive of the new asset, on the date of transfer of the original asset, or

- You purchase any residential house other than the new asset, within 1 year after the date of transfer of the original asset, or

- You construct any residential house other than the new asset, within 3 years after the date of transfer of the original asset.

- The income from a house property, other than the one owned on date of transfer of original asset is chargeable under the head “Income from house property”.

- You purchase a house (other than new asset) within 2 years or construct a house (other than new asset) within 3 years after transfer date of original asset and the income from such a house is chargeable under the head “Income from house property”.

- You sell the new asset within 3 years from date of its purchase or construction (as the case may be).

Capital Gains Account Scheme

After selling the original asset and until you purchase a residential house property (new asset), you can deposit your sale proceeds in a dedicated account called as Capital Gain Account. Amount deposited in Capital Gain Account is not taxable until 2 years (if you purchase a house) or 3 years (if you construct a house) from the date of transfer of original asset.

Please note that if you do not invest in a residential house in the financial year in which the original asset is sold, you should deposit sale proceeds from your original asset in the CGAS account before the last date of filing IT returns for the particular financial year.

Check out this detailed guide on Capital Gain Account to learn about types of CGAS accounts, the process of opening an account and other details about CGAS account.

Latest amendment to Section 54F of Income Tax Act

An amendment to section 54F of Income Tax Act was introduced in Budget 2014 according to which starting Financial Year 2014-15, exemption under section 54F will be available only if the net consideration from the sale of original asset is re-invested in 1 residential house property in India.

Over to You

We need your love! Like and Share this article on “Section 54F of Income Tax Act 1961 – Decoded”, if you found it useful.

Have something to say or ask? Please comment below.