If you are planning to purchase an under construction house with the help of a home loan, you would come across terms such as Pre EMI, Pre EMI interest, EMI under construction, moratorium period etc. For an under-construction property, the most preferable payment plan is construction linked plan in which the bank would disburse loan as per the construction schedule. In such cases, the bank will give you an option of choosing between Pre EMI or full EMI repayment schemes. Most people do not do proper analysis and they blindly go with the Pre EMI option. But is this really beneficial to you? In this article, we will explain to you in detail about Pre EMI and full EMI options, so that you can decide yourself, which option is better for you.

Following topics are covered in this guide:

- What is Pre EMI?

- EMI Under Construction

- Pre EMI vs EMI

- Subvention Schemes

- Tax Considerations

What is Pre EMI?

A Pre EMI is a repayment scheme offered by banks for under construction properties, in which you would be required to pay only the interest portion on the amount disbursed, till entire loan amount is disbursed. The time period for which you will not be required to pay the principal amount is called moratorium period.

What is Pre EMI interest?

The interest amount, payable monthly, in a Pre EMI repayment scheme is called as Pre EMI interest. Generally, the banks will offer the Pre EMI interest option until the entire loan is disbursed or upto the maximum moratorium period, whichever happens first. After the moratorium period, you will be required to pay full EMI, whether the construction is completed or not. Generally, banks allow a maximum moratorium period of 3 years for under construction properties.

EMI Under Construction (Full EMI)

EMI under construction or full EMI is an alternative repayment scheme for home loan on under construction properties. In this scheme, you can start paying full EMI for a partly disbursed home loan. This scheme is helpful for those who want to pay off their loans fast as when you pay full EMI, you will be paying higher amount of principal amount. By the time your property is completed, you would have already paid a decent amount of your loan.

Pre EMI vs EMI

When you buy an under construction property using a home loan, which option would you choose, Pre EMI or EMI? A low monthly outgo towards EMI does not necessarily mean that it is the best option for you. You should first analyze your situation and then choose between Pre EMI and EMI options.

An Illustration

Let us understand the comparison of Pre EMI vs EMI with the help of an example.

Suppose you booked an under construction property @ Rs. 65 lakhs. You paid Rs. 15 lakhs as initial down payment and for the balance amount you are taking a home loan of Rs. 50 lakhs @ 10% interest rate with a tenure of 20 years. Now, the bank is asking you to choose between Pre EMI and full EMI.

Let us assume that the construction period is 2.5 years (30 months) and after the initial down payment the bank will disburse Rs. 10 lakhs every 6 months till the construction is completed.

Using the EMI Calculator, you can calculate the EMI (for Rs. 50 lakhs loan for 20 years @ 10%) as Rs. 48,251.

Following will be the Pre EMI schedule during construction:

| Time from booking | Stage | Amount Disbursed (Rs.) | Pre EMI (Rs.) |

| 6 months | On completion of foundation | 10 lakh | 8,333 |

| 12 months | On completion of third floor | 10 lakh | 16,667 |

| 18 months | On completion of sixth floor | 10 lakh | 25,000 |

| 24 months | On completion of Structure | 10 lakh | 33,333 |

| 30 months | On completion of Finishing Works | 10 lakh | |

| Total Pre EMI Interest | 500,000 | ||

After the possession of house i.e. after last disbursement, you will start paying full EMI of Rs. 48,251 in case of Pre EMI option.

While, in case of EMI under construction option, you will start paying full EMI immediately after first disbursement of Rs. 10 lakhs.

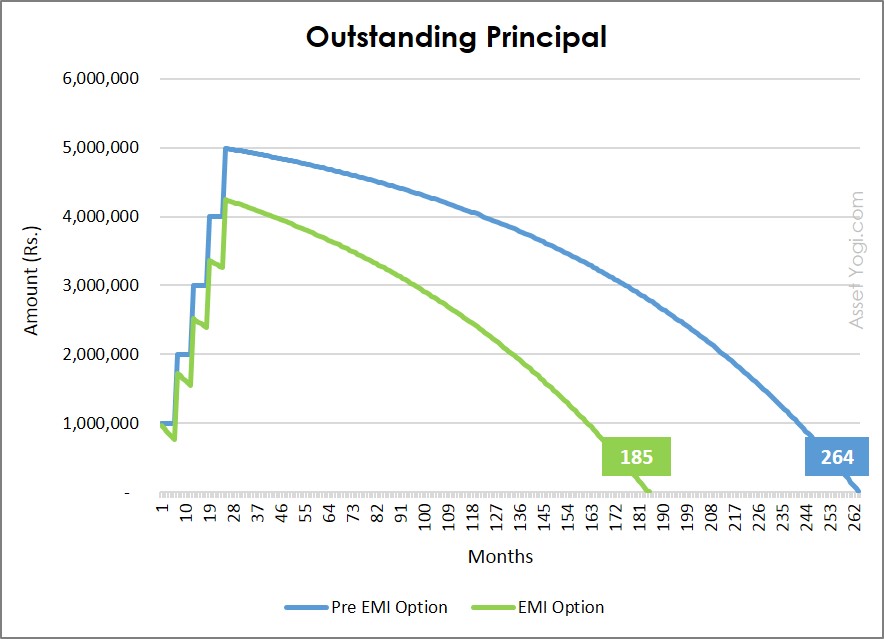

Now to have a better visualization, let us compare Pre EMI vs EMI with the help of graphs. First, let us analyze the outstanding principal & loan tenure.

Outstanding Principal – Pre EMI vs EMI

As you can see in the graph, if you take the EMI option, you can pay your loan in 185 months i.e in about 15.5 years. While, if you take the Pre EMI option, you will pay your loan in 264 months or 22 years i.e. 2 years while paying Pre EMI interest during construction and then 20 years while paying full EMI.

It is clear from the graph that you can pay your loan much faster in case you start paying full EMI immediately after first disbursement of loan i.e. almost 6.5 years before.

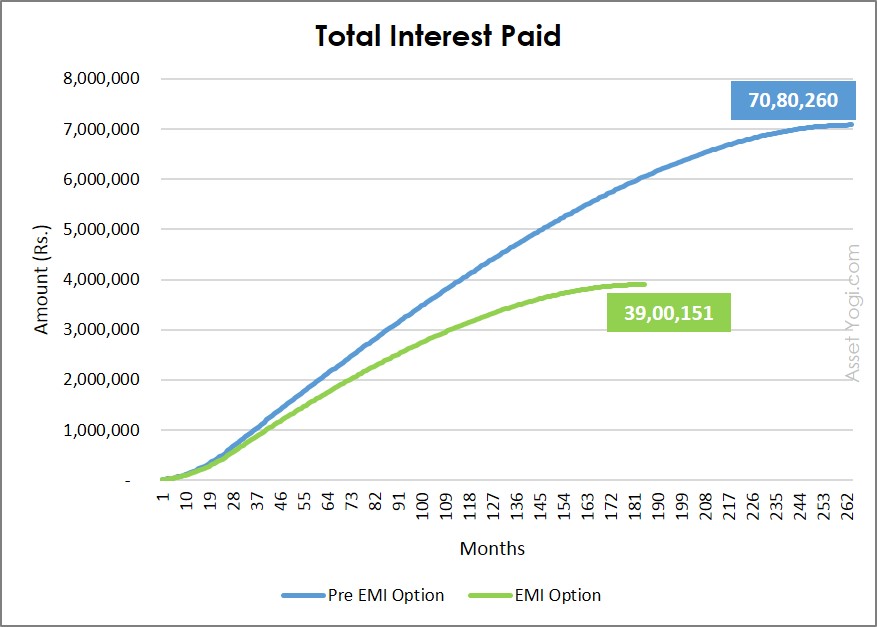

Now, let us compare total interest paid in both cases:

Total Interest Paid – Pre EMI vs EMI

As is clear from graph, the total interest paid in EMI option is Rs. 39 lakhs, which is much lower than the Rs. 71 lakhs in Pre EMI option.

Therefore, it is clear from the calculations that EMI option is better than Pre EMI option as far as savings are concerned. However, there can be other reasons for which you may prefer the Pre EMI option. Let us see which option is better in what situation.

Pre EMI or EMI – Which one to choose?

You should choose EMI option, if:

- You want to close your loan faster.

- You want to reduce your interest burden.

- You do not have time or interest to analyze and invest in other alternative investments.

You should choose Pre EMI option, if:

- You can make higher returns (more than the home loan interest rate) by investing your surplus money in alternative investments.

- You want to sell the property before the construction is complete.

- Your finances are tight at the moment and you expect a salary raise before possession.

- You are staying on rent currently and find it difficult to afford both EMI and rent together.

Subvention Schemes – Builder pays Pre EMI

These days, many builders collaborate with banks and financial institutions to offer even more convenient payment options to customers. They will ask you to pay a minimum amount upfront and balance on possession. But what is the catch in such schemes?

Behind the scenes of 20-80 / 10-90 Schemes

Under subvention schemes, builder will ask you to pay 10-30% cost upfront and balance amount on possession. You will be raising home loan on your house but the builder will pay the pre emi interest on your behalf to the bank. Though the option may look attractive, the catch here is that the price of the property is increased by the builder to take care of the interest portion during construction. This means that the builder indirectly gets cheaper financing for his project.

In many cases, the builder may have an arrangement to raise the entire loan amount upfront. This is where you should be a little careful. Once, the builder gets cheaper funds all upfront, there is no incentive for him to complete the project in time. He may divert those funds to buy more land instead of completing the project. You should be really cautious when you invest in subvention schemes.

Tax Considerations

Whether you choose Pre EMI or EMI option, you can claim deduction on the interest paid during construction (IDC) under section 24 of IT Act. You can claim tax deduction on IDC only after you get the possession of your house in five equal installments over 5 years. For example, if your total interest amount during construction was Rs. 3 lakhs, you can claim deduction on Rs. 60,000 per year for first five years from the date of possession.

You cannot claim deduction on the principal amount paid during construction. So, if you choose EMI under construction option, you will not get any tax advantage. If you want to pay your loan faster, you should choose full EMI option irrespective of the tax considerations.

To know more about tax benefits, read our article on Home Loan Tax Benefit.

We hope that now you would be able to decide between Pre EMI and EMI, for your situation.

Over to You

We need your love! Like and Share this article on “Pre EMI Guide – What is Pre EMI Interest – Pre EMI vs EMI”, if you found it useful.

Have something to say or ask? Please comment below.